Are you tired of living paycheck to paycheck and feeling like you’re not making any progress towards your financial goals?

It’s frustrating when you work hard every day, but still struggle to make ends meet. You might wonder if there’s something you’re missing, or if you’ll ever be able to build real wealth.

The truth is, your wealth depends on what you do on payday. Don’t believe me? Keep reading.

In this post, I’ll share my practical tips on how to manage money wisely on payday and build a solid financial foundation for the future.

Table of Contents

How to Manage Money Wisely To Maximize Your Wealth

My wife and I are huge college sports fans.

The problem is, we’re not on the same team.

She’s a die-hard Michigan State fan, which makes sense since she got her undergrad degree there. I’m an Ohio State Buckeye, and although I didn’t attend that school, both my Uncles, Dad, and my first cousin, Jason, did.

So their intense love for OSU sports became ingrained in me from an early age. Matchups between both schools have traditionally been pretty intense in our house. And both the boys are divided on their allegiance.

For several years we would stay at Jason’s house and then head in early Saturday morning to tailgate on football game day. They were such intense fans they bought an old school bus for the sole purpose of converting it to a Buckeye tailgating experience. Good times.

Jason was merciless to Kara when the Buckeyes won, which of course, I don’t condone any trash talk in competitive environments (wink wink). Poor thing. But she willingly entered the lion’s den, so that was on her.

In one of our visits, they had just purchased a huge, beautiful home in an expensive suburb of Columbus. It was right on a private golf course, and his wife had just given him the green light to join. On the Sunday following a Buckeye win, we headed over to their new lake home, to wakeboard on their new powerboat.

We rode over in their new car, which we came to find out was Kirk Herbstreit’s car that he had just turned into at the dealership. Herbstreit is a very popular ESPN college football analyst with a taste for expensive cars. When we were departing Monday morning, they were packing up and heading to an expensive resort in the Caribbean.

At the time, these things they were buying made sense to me. Jason was a Controller at a corporation, and his wife was a successful pharmaceutical sales rep. I can’t imagine any scenario where they were earning less than $500,000 per year, combined. I would not be surprised if it were more than that.

Since then we have parted ways, but what did surprise me to hear very recently was that they were financially broke!

I am well aware as a wealth strategist that many high earners spend everything they make. I did, however, have a hard time believing with that high an income that they could possibly be in financial trouble.

The bottom line is that regardless of your income, if you continually buy liabilities and ignore the accumulation of assets, it catches up to you. What if they had stayed in their starter home, rented a lake house for a week or two, prepared and cooked at home, played the public golf course, and bought reliable used cars?

This is what we did while we were earning a multi-six figure income. It’s quite sustainable.

What if they took those savings and bought rental property, quality stocks, private businesses, crypto, and hired wealth coaches? The story ends quite differently now. They’d be multi-millionaires. Easily.

What the Poor, the Middle Class, and the Wealthy do on Payday

Payday can be any event where income flows into your life – whether it be from a W-2 job, a 1099 contract payment, a commission from a sale, profit from buying and selling a product, or income from an investment.

Also, let’s get this clear. I do not make the categories. The categories are where your habits, your behavior, and your mindset places you. You’re not doing certain things because you’re poor. You’re poor because you’re doing certain things.

Let’s look at what the poor, the middle class and the wealthy do differently.

#1. Don’t make impulse purchases

The poor go and buy stuff. If it’s on sale then that means it’s a deal and they’ll need to buy it. They will typically spend everything they have before their next paycheck comes in, giving them no margin for error if anything should go wrong.

When the tire goes flat and will cost $400 that they don’t have, this is incredibly bad luck that they can’t believe happened to them, instead of a minor life event that’s routine and typical and is expected.

#2. Avoid getting sucked into gambling

Gambling is also big among the poor. Slot machines, lottery tickets, keno, these games with extreme odds stacked against them are their entertainment of choice. They are also very susceptible to predatory lending, paying huge amounts towards high interest loans, and giving out paycheck cash advances.

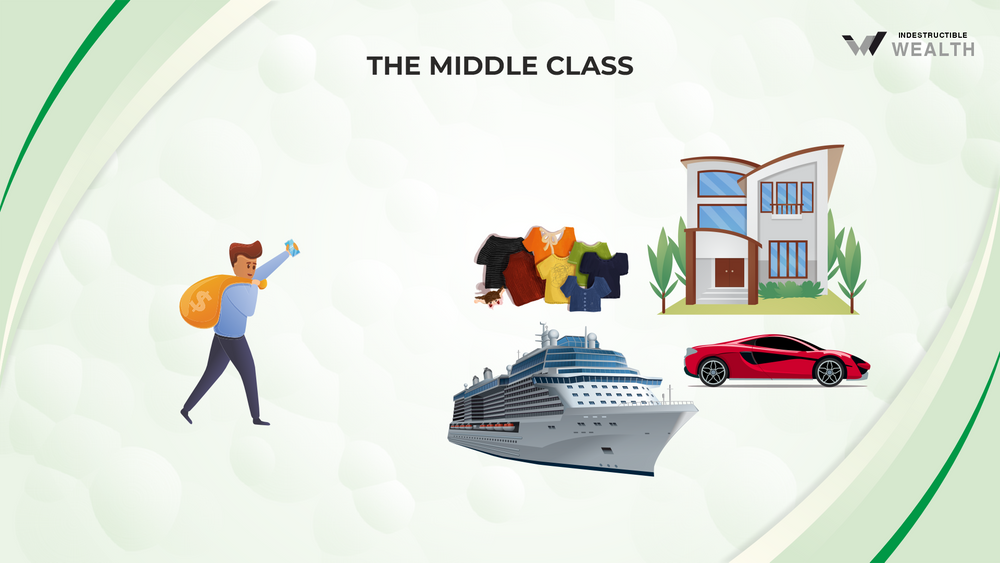

#3. Don’t spend everything you earn

The middle class buy liabilities on payday. We define a liability as “something that costs you money”. They may earn a very good income, but income doesn’t put you in the wealthy category.

They buy the expensive car, get a bigger house, buy the boat, the snowmobile, the motorcycle, take the expensive vacation, remodel their basement or kitchen, join the country club, and rack up a monthly loan payment that eats up their entire paycheck as fast as it comes in.

They’ll take out a HELOC and instead of buying an asset that just went on sale, they’ll tap it out for consumption then have another monthly loan payment. If they earn $10,000 per month, then they will have $10,000-$12,000 in monthly expenses. It doesn’t matter that much if they get a raise or increase their sales – they will always raise their spending to match their income.

The middle class chase the rich lifestyle, the wrong way.

So what do the wealthy do differently?

What the wealthy do on payday is the difference maker when it comes to learning how to manage money wisely.

They buy income. Sounds oxymoronic?

What I mean by buying income is they buy assets, which we define as “something that pays you”.

No, we aren’t talking about your personal residence, that doesn’t pay you unless you also rent it out and it creates positive cash flow. The wealthy reinvest their money back into their own businesses to increase revenue and the income they can expect in the future.

They buy cash flowing real estate, dividend stocks, bonds, private businesses, structure private money loans, mortgage backed notes, RV parks, and alternatives like income producing cryptocurrency.

It’s not that they don’t spend money and buy large homes, expensive cars, take amazing vacations or buy expensive toys. They definitely do these things and they very much want to enjoy their money. The difference is simply in the order in which they do it.

What’s my approach to managing money wisely?

I, in fact, buy all of the above things. I actually very much enjoy spending money. However, I don’t enjoy spending the seed, I really only enjoy spending it when it’s the harvest. In other words, I want my capital put to work generating additional income, and THEN I’ll go out and get stupid.

When the Cleveland Indians played the Chicago Cubs in the World Series, I got a ticket behind 1st base for $4500. I took the rental income from my property portfolio to fund it. In 2018, I played in the World Series of Poker Main Event, a lifelong dream that started back in my college dorm room days playing for quarters with my friends.

That entry fee is $10,000, and certainly, that’s a terrible bet as statistically, I had very little chance. I didn’t win; in fact, I got knocked out the first day, but I will always treasure the experience (and give it a few more tries!).

When I turned 40, I threw a 2-night party with entertainment and an open bar with full apps, to the tune of $15,000. Our family takes at least 2 weekend ski trips each winter up north in Michigan to Boyne Mountain, after hotel, lift tickets, rentals, lessons for the boys, and resort food for a family of 4 for 3 days, we routinely drop $3-$4k.

And last year, I surprised my wife with a new 4-carat rock on our wedding anniversary. She has to put up with me and my bullshit so she definitely deserves the finest. All of these purchases certainly could be considered irresponsible and frivolous, but I do not regret any of them, because the income from my investments paid for all of them! And then that money will be replenished in short order.

It’s the order in which the wealthy do it.

When payday hits, I absolutely look forward to getting a dopamine hit (feel good chemical in your brain) from buying more assets. I’ve trained my brain to get a dopamine hit because I know that I’ll be able to get more and much better items, have more fun, take more trips, and have a much better lifestyle if I simply switch the timing of what I purchase.

What I’ve personally seen happen is not a double increase – I’ve seen a triple, quadruple, and even greater compound effect where I can now consume exponentially more goods and services from simple decisions and disciplines on payday!

Final Thoughts

Building wealth isn’t just about how much money you make, but also about what you do with it on payday. Whether you’re poor, middle class, or wealthy, your financial habits and mindset play a significant role in your long-term financial success. That’s why it’s so important to learn how to manage money wisely.

Poor financial decisions, such as impulsive purchases, gambling, and living paycheck to paycheck, can keep you trapped in a cycle of financial struggle. Meanwhile, the middle class often fall into the trap of buying liabilities instead of assets and failing to save and invest for the future.

To maximize your wealth, it’s important to adopt wise financial habits such as avoiding impulsive purchases, steering clear of gambling, and not spending everything you earn. Investing in assets like rental properties, quality stocks, and private businesses, and hiring a wealth coach can also make a major difference in your long-term financial success.

Don’t let your paycheck go to waste. Take control of your finances, make wise financial decisions on payday, and build a solid financial foundation for your future.

Whenever you’re ready, there are 3 ways I can help you level up your finances:

- Take an affordable self-learning e-course: COMING SOON

- Take our new interactive course The Indestructible Wealth Academy to help you buy ten cash flowing properties within two years, with the goal to create a million in equity: COMING SOON

- Ready to invest your money?

→ Buy cash flowing, turnkey real estate. It’s acquired, renovated, and managed for you by my company, High Return Real Estate.

→ Wish you had bought bitcoin back at $12,000? Now you can with my company Simple Crypto Mine. We provide the machines, the hosting, the technical expertise, and the maintenance. Watch bitcoin drop in your wallet every five days for another stream of passive income. Email me at [email protected] to request the investor packet.

→ Are you an Accredited Investor with larger amounts of capital to invest? Syndicated deals in self-storage and car washes are 100% passive and very lucrative. Email me at [email protected] to request the latest investor replay to learn more!